There are many parameters that a company’s management is assessed and evaluated on. Some of the parameters are based on financial statement ratios, customer satisfaction, and employee satisfaction. One of the financial statement ratios that can be used to assess the overall operating health of the company is a cash conversion cycle. A cash conversion cycle could provide management with useful information about where improvements could be needed. It’s also a very easy ratio to calculate.

What is cash cycle and what does it tell you?

A cash cycle measures how many days it takes a company to convert “cash out” into “cash in”. For some of you, it may not make sense, and you’ll ask me how “cash out” can be converted into “cash in”. Well, if you think about a typical manufacturing cycle, you’ll see that the first stage of production is expending cash for inventory. After that, it will take some time to manufacture/assemble the final product. Then the product needs to be sold to a customer. Once the sales are made, it will take time to collect cash from the customer if it is a credit sale.

As a result, the company does not have access to this cash from the time the inventory vendor was paid, until they collect payment from their customer. A cash conversion cycle shows the number of days it takes the company to convert cash paid for inventory, into cash collected from customers.

How is cash conversion cycle calculated?

There are three different cycles that are included in a cash conversion cycle – days inventory outstanding, days sales outstanding, and days payables outstanding. A cash conversion cycle is days inventory outstanding, plus days sales outstanding, minus days payable outstanding. The three ratios are calculated as follows:

- Days Inventory Outstanding = Avg. Inventory / (COGS / 365)

- Days AR Outstanding = Avg. AR / (Sales / 365)

- Days AP Outstanding = Avg. AP / (Inventory Increase + COGS) / 365)

Cash cycle is simply the sum of the first two ratios minus the third.

What should you do with this number and what does it tell you?

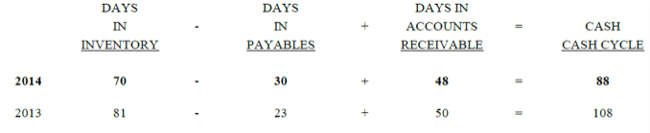

First off, a cash conversion cycle, as well as, individual ratios that go into the calculation, must be compared from one period to another, to identify any significant swings. For example, in comparing annual ratios you noticed that the cash conversion ratio decreased from 108 days to 88 days, as detailed in the table below. It tells you that for various reasons it takes 20 fewer days to convert cash expended for inventory into cash collected from customers. This fact indicates a dramatic improvement inefficiencies in inventory management, AR collection, or AP disbursements areas.

In addition to comparing cash conversion ratio internally from period to period, management should benchmark it against other companies in similar industries. Your ratios may be consistent from period to period, but you may not realize that industry wide averages vary differently from your company’s cash conversion ratio. Discovering this fact may be forcing the company to look at its internal cash flow and reevaluate its processes to identify any potential problems. At the same time it may open up a window of opportunities for operational improvements, which may result in increased profitability.

As demonstrated above, a cash conversion cycle could be a very useful management tool to evaluate and assess operating health and effectiveness of a company’s operations, and implement needed improvements to help the company convert cash faster and more efficiently.